SEC Adopts Final Climate-Related Rules

On March 6, 2024, in a 3-2 vote during an open meeting, the Securities and Exchange Commission (SEC) adopted the long-awaited final rules on climate disclosures that require public companies to “provide certain climate-related information in their registration statements and annual reports.”[1] In its adopting release, the SEC explained that the final rules’ purpose is to provide “consistent, comparable, and reliable information about the financial effects of climate-related risks on a registrant’s operations and how it manages those risks while balancing concerns about mitigating the associated costs of the rules.”[2] The SEC also pointed out that, although many registrants already provide some of the required disclosures under the final rules, such as greenhouse gas (GHG) emissions-related disclosure, the final rules will ensure that standardized disclosure is applied to all registrants, facilitating comparability and transparency of such disclosures to investors.

The SEC postponed issuing final rules on climate-related disclosures many times since it issued the proposed rules in March 2022, which garnered thousands of comments. The final rules ended up including significant cutbacks to the initial proposed rules. Most notably, the final rules removed Scope 3 disclosure requirements and board of directors’ climate-related risk expertise disclosure requirements. SEC Chair Gary Gensler also stated in his open meeting remarks that disclosure requirements under the final rules will be rooted in materiality. Materiality, however, is “not determined merely by the amount of these emissions; [r]ather, as with other materiality determinations under the Federal securities laws and Regulation S-K, the guiding principle for this determination is whether a reasonable investor would consider the disclosure of … Scope 1 emissions and/or its Scope 2 emissions, important when making an investment or voting decision or such a reasonable investor would view omission of the disclosure as having significantly altered the total mix of information made available.”[3]

Final Rules Disclosure Requirements.

The final rules will require registrants to provide both qualitative disclosures on climate risk, risk management, corporate governance and certain targets and goals, as well as quantitative disclosures of GHG emissions and climate-related expenditures. Generally, the final rules will require disclosures on Scope 1 and 2 GHG emissions, if material, and the relationship between the registrant’s climate expenditures, strategy, transition plans and target disclosures and any applicable material climate risks and impact on the registrant’s operations.

Some key points and requirements under the final rules’ are further discussed below.[4]

- Climate-Related Disclosures.

Registrants will be required to discuss whether and how any climate-related risks identified by the registrant has materially impacted, or is reasonably likely to materially impact, its business model, results of operations or financial condition. These disclosures should include actual and potential material impacts of both physical and transitional risks, such as increased expenses as a result of transition plans or potential adoption of new governmental regulations and policies, technologies to mitigate or to adapt to climate-related risks and other general trends applicable to the registrant.

Additionally, registrants will need to disclose material expenditures incurred as a result of the integration of climate-related risks into the registrant’s overall business strategy, financial planning and capital expenditure allocation, including how established targets and transition plans are considered by the registrant. These disclosures are also both quantitative and qualitative in nature. The quantitative disclosures should include the actual expenditure costs incurred, material impacts on financial statements and assumptions made in connection with climate-related risk mitigation and adaptation. Qualitative disclosure should include details of any transition plans in place, narrative related to potential scenarios and their corresponding impact to the registrant, risk management system or processes to address such risks, and other targets or goals disclosure and how such measures have, or are likely to, materially affect the registrant’s results of operations, financial condition and business (e.g., the scope of activities included in the target measures, the unit of measurement, intended date of achieving such targets, and narrative as to how the registrant intends to meet its established targets and goals).

- GHG Emission Disclosures.

Non-exempt large accelerated filers (LAFs) and accelerated filers (AFs) will be required to disclose Scope 1 and/or Scope 2 GHG emissions, if such disclosures are considered material to the registrant. The required disclosures include: (i) direct GHG emissions in terms of CO2e from operations that are owned or controlled by a registrant; (ii) indirect GHG emissions from generation of purchase or acquired electricity, steam, heat or cooling that is consumed by operations owned or controlled by the registrant; and (iii) if the registrant is required to disclose the foregoing items (i) and (ii), then it must also disclose its methodology and significant inputs and assumptions used to calculate such GHG emission metrics.

Further, subject to phase-in periods (see discussion and Annex A below), LAFs and AFs will also be required to provide and attach to their filings an attestation report providing limited or reasonable assurance, as applicable, on their GHG emissions disclosure in the relevant filing.

- Financial Disclosures.

A new Article 14 to Regulation S-X will require a note in audited financial statements, which will disclose climate-related financial impacts, subject to certain impact thresholds[5], that will include: (i) capitalized costs, expenditures expenses, charges and losses incurred as a result of severe weather events, other natural conditions and transition-plans, and, if this financial note disclosure is required, then it must also provide context about how such effect and measures were derived; (ii) financial impacts and accounting policy related to carbon offsets or renewable energy credits, if material to the registrant’s plan to achieve its climate-related targets or goal; and (iii) how a registrant’s estimates and assumptions to produce its financial statements were materially impacted by risks and uncertainties related to severe weather events and other natural conditions, or any disclosed climate-related targets and transition plans.

Phase-In Periods and Applicability of Final Rules.

The final rules included several accommodations and included phase-in periods, along with exemption for certain registrants, to its climate-related rules. These include exemption for smaller-reporting companies (SRCs) and emerging growth companies (EGCs) from GHG emission disclosure requirements, delayed disclosure requirements for registrants required to provide Scope 1 and/or Scope 2 disclosures and a safe harbor from private liability for climate-related disclosures about transition plans, scenario analysis, use of an internal carbon price and a registrant’s targets and goals other than disclosures that are historical facts.

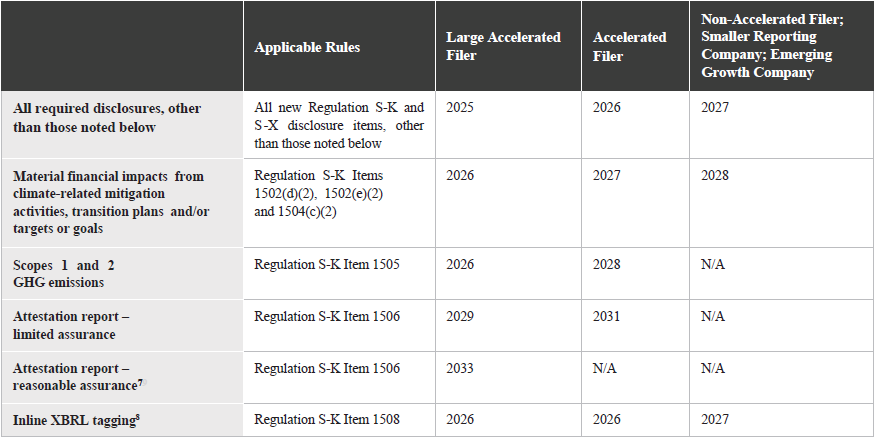

The table included below in this alert under Annex A summarizes the phase-in periods and applicability of rules to LAFs, AFs, SRCs and EGCs. The final rules will become effective 60 days after date of publication in the Federal Register.

How to Prepare and Next Steps.

Many registrants already incorporate climate-related disclosure to some extent in their SEC filings or through voluntary reports. While there have already been legal challenges to these final rules[6], and we expect more to come, registrants should nevertheless initiate the development of their implementation plans for these new reporting requirements and consider the following:

- Review Current Disclosure. Registrants should review the existing climate-related disclosures in their SEC filings and other publicly disclosed information, and adjust as needed to the final rules.

- Assess Processes and Controls. Registrants should evaluate how current climate-related information is compiled and assessed by management and its board of directors, and analyze the existing processes and controls for both the quantitative and qualitative components of the final rules.

- Enhance Governance and Reporting Systems. Registrants should update disclosure controls and procedures concerning GHG emissions and other mandated climate disclosures as necessary to adhere to the new rules requirements, in terms of both financial statements and general disclosures.

- Review Board of Directors’ Oversight. Assess the current framework for the board of directors or committee, if applicable, oversight of climate-related issues, risks and uncertainties, and examine whether any corporate governance document – e.g., a committee’s charter – should be adjusted to reflect any additional roles or responsibilities by the board of directors or such committee.

- Consider Materiality of GHG Emissions and Climate-Related Risks. Initiate an assessment of the materiality of the registrant’s Scope 1 and Scope 2 GHG emissions, and consider whether such information is material and required to be disclosed. Registrants must continuously evaluate its climate-related risks and their potential impacts on the business, results of operations and financial condition.

- Identify Targets and Goals. Registrants should review their established or new climate-related targets and goals, and be prepared to disclose them if material to the registrant’s business.

- Consider Impact of Disclosure. Registrants should begin evaluating the potential benefits of preparing preliminary draft of climate-related disclosure as early as possible to refine the disclosure approach and have outside counsel review such disclosures to ensure compliance with the rules; test internal controls and procedures; or make operational adjustments, if necessary.

- Prepare for Attestation. Registrants should be familiar with the upcoming requirements to provide attestations, if applicable, and consider the additional support and services registrants may require, and third-parties it may need to engage. Registrants that anticipate needing to include attestation reports should begin engagement discussions with providers as early as this year.

Please contact the Mitchell Silberberg & Knupp Corporate & Business Transactions Department to discuss how we can help you prepare to and comply with the new SEC climate-related disclosure obligations.

ANNEX A

[1] https://www.sec.gov/files/33-11275-fact-sheet.pdf

[2] https://www.sec.gov/news/press-release/2024-31

[3] https://www.sec.gov/files/rules/final/2024/33-11275.pdf

[4] The disclosures discussed above refer to the adopted Regulation S-K Items 1500(a); 1501; 1502(a), (b) and (c)-(g); 1503; 1504; 1505(a) and (b); 1506; 1507; as well as Regulation S-X Articles 14-02(a), (c), (d), (e), (f) and (h).

[5] No disclosure of expenditures expensed as incurred and losses is required if the aggregate amount is less than (i) 1% of the absolute value of income or loss before income tax expense or benefit, or (ii) $100,000 for the relevant fiscal year, and no disclosure of the absolute value of capitalized costs and charged is required if the aggregate amount is less than (a) 1% of the absolute value of stockholders’ equity or deficit at year end or (b) $500,000 for the relevant fiscal year.

[6] On March 15, 2024, a federal court temporarily halted the new rules from the SEC based on the lawsuit brought by two fracking companies, Liberty Energy and Nomad Proppant Services. In their lawsuit, they claimed that the SEC rules were “arbitrary and capricious” and that they violated the First Amendment by essentially mandating discussions over climate change, in addition to causing certain public companies to comply with significantly higher compliance costs.

ANNEX A

[7] Years in the table reflect any fiscal year beginning in the calendar year listed. For

example, a large accelerated filer with a December 31 fiscal year end would be required to comply with the earliest disclosure requirements beginning with its annual report for fiscal year ending December 31, 2025 (filed in 2026).

[8] Financial statement disclosures under new Regulation S-X Article 14 will be

required to be tagged in accordance with existing rules pertaining to the tagging of

financial statements.